Thailand LTR Visa vs. Retirement Visa: Which Is the Right Choice for You in 2026?

— THAILAND IMMIGRATION · JUNE 2026

For anyone planning long-term residency in Thailand, choosing between the Non-Immigrant O Retirement Visa and the Long-Term Resident (LTR) Visa is one of the most consequential immigration decisions you will make — and the right answer depends entirely on your financial profile, family situation, and long-term goals.

BY WARUS & JAMES RAYDAR INTER LAW ·THAILAND IMMIGRATION

Thailand has long been one of the world's most popular destinations for long-term expatriates, retirees, and internationally mobile families. Its combination of high quality of life, affordable cost of living, excellent private healthcare, and warm climate makes it an enduringly attractive relocation destination — particularly for citizens from the United States, the United Kingdom, Europe, and Australia.

In recent years, Thailand's immigration framework has evolved significantly. The introduction of the Long-Term Resident (LTR) Visa in September 2022 — administered by Thailand's Board of Investment (BOI) — created a fundamentally new option for high-net-worth individuals and qualifying retirees seeking genuine long-term stability in the country. For many, the question is no longer simply "how do I retire in Thailand?" but rather "which pathway best serves my family and financial interests over the next decade?"

This guide sets out a comprehensive, legally informed comparison of both routes — examining eligibility, duration, financial requirements, family provisions, tax implications, and practical administrative burdens — so that you can make an informed decision before engaging legal counsel.

Understanding the Two Pathways

The Non-Immigrant O-A / O-X Retirement Visa

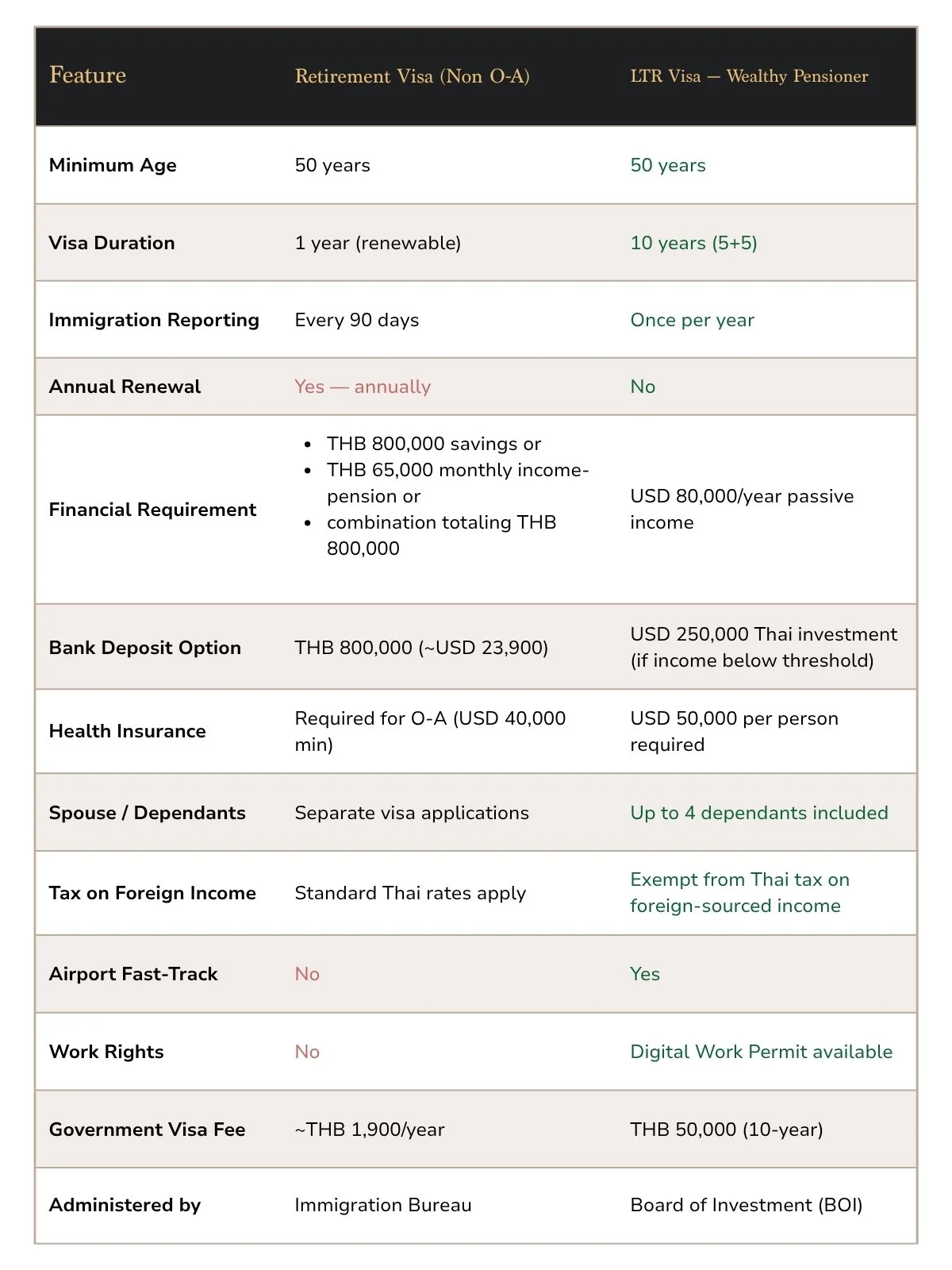

The Non-Immigrant O-A(Retirement) Visa has existed in various forms for decades and remains the most widely used long-stay option for retirees in Thailand. It is issued initially for 90 days or one year, and can be renewed annually at a local Immigration office in Thailand, provided the applicant continues to meet the financial requirements.

To qualify for the standard Non-O-A Retirement Visa, applicants must be aged 50 or above and satisfy one of the following financial criteria: savings of at least THB 800,000; monthly income or pension of at least THB 65,000; or a combination of savings and income totaling at least THB 800,000. Upon annual extension, applicants must continue to satisfy one of these financial requirements, including maintaining at least THB 800,000 held in a Thai bank account, monthly income or pension of at least THB 65,000, or a combination totaling at least THB 800,000 per year. There is no investment requirement, no BOI involvement, and the process can be managed through a local Thai Immigration office or a Royal Thai Embassy or Consulate abroad.

The appeal of the Retirement Visa lies in its relative accessibility and the simplicity of its initial setup. However, it comes with a number of ongoing administrative obligations that many retirees find burdensome over time — most notably the requirement to report to Thai Immigration every 90 days and to renew the visa annually with fresh financial evidence.

The LTR Visa (Wealthy Pensioner Category)

The Long-Term Resident Visa is a fundamentally different product — a premium, BOI-administered residency programme designed to attract high-value individuals to Thailand over a 10-year horizon. The Wealthy Pensioner category within the LTR programme is specifically designed for retirees aged 50 and above who hold qualifying passive income or a combination of passive income and Thai-based assets.

To qualify under the Wealthy Pensioner stream, applicants must meet one of two financial thresholds: a passive income — from pensions, annuities, dividends, interest, or rental income — of at least USD 80,000 per annum; or a passive income of between USD 40,000 and USD 79,999 per annum combined with a qualifying investment in Thailand of not less than USD 250,000 which may include government bonds, foreign direct investment, or registered Thai property.

In addition to the income or asset threshold, all LTR applicants must hold qualifying health insurance coverage of at least USD 50,000 per person, inclusive of treatment in Thailand, with at least 10 months of coverage remaining at the time of application.

“The LTR Visa is not simply a longer version of the Retirement Visa. It is a structurally different residency instrument — one that trades a higher entry threshold for a decade of stability, reduced administrative burden, and meaningful tax advantages.”

Side-by-Side Comparison

The Tax Advantage — A Factor That Changes the Calculation

One dimension that is frequently underappreciated in visa comparisons is the tax treatment of foreign-sourced income. Thailand updated its tax rules in 2024, making foreign income remitted into Thailand in the same tax year it is earned potentially assessable for Thai income tax — regardless of visa type.

However, LTR Visa holders in the Wealthy Pensioner category enjoy a specific statutory exemption from Thai personal income tax on their foreign-sourced income. This is not a grey area or a planning position — it is an explicit benefit of the LTR programme, established by Royal Decree and confirmed in the BOI's programme documentation.

For a retiree living on USD 80,000–150,000 per year in passive income and remitting funds to Thailand regularly, this exemption can represent a tax saving of tens of thousands of dollars annually. For high-income retirees, the financial benefit of the LTR Visa's tax exemption alone can exceed the entire cost of the application — including legal fees, government fees, and health insurance — within the first year of residency.

Retirement Visa holders enjoy no equivalent protection. If they spend more than 180 days per calendar year in Thailand — which the vast majority of long-term residents will — they become Thai tax residents and are subject to Thai progressive income tax rates on assessable foreign income remitted into Thailand.

Administrative Burden — The Hidden Cost of the Retirement Visa

The 90-day reporting obligation under the Retirement Visa is more significant than it might first appear. Every 90 days, the visa holder must either present in person at a Thai Immigration office, submit a postal notification, or — where available — file online. Failure to report on time results in a fine of THB 2,000 per occurrence. Over a 10-year period, this amounts to 40 mandatory interactions with the immigration system.

Similarly, annual visa renewal requires fresh bank statements, income evidence, and completion of TM.7 and TM.30 forms, often with in-person attendance. For internationally mobile retirees — those who travel frequently between countries — managing the renewal window and maintaining continuous compliance can become a genuine logistical challenge.

The LTR Visa replaces annual extension applications with a long-term residence framework, granting an initial five-year stay that may be renewed for a further five years, subject to continued qualification. Combined with a single annual address report, this significantly reduces the administrative burden associated with traditional retirement-based immigration categories. For retirees seeking long-term stability, convenience, and predictability in Thailand, the LTR Visa offers a compelling alternative.

Which Pathway Is Right for You?

Choose the LTR Visa if

Your passive income exceeds USD 80,000 per year — or you hold USD 250,000 or more in qualifying Thai assets alongside USD 40,000+ annual income.

You are relocating with a spouse and/or children and want the entire family covered under a single application umbrella.

You intend to remit significant foreign income into Thailand and want legal certainty over your tax position.

You value long-term stability and want to avoid the annual renewal cycle of the standard Retirement Visa.

You are planning a permanent or near-permanent relocation and want a 10-year framework to build your life around.

The Retirement Visa may suit you better if

Your passive income falls below the USD 40,000 LTR threshold and you do not hold significant Thai assets.

You are relocating alone and do not have dependant family members to include.

You prefer a lower initial financial commitment and are comfortable with annual renewal.

You are in a transitional phase and intend to build toward LTR eligibility over the coming years.

A Note on Legal Advice

The comparison above provides a general framework, but the right decision for your circumstances depends on a precise assessment of your income structure, the nature and jurisdiction of your assets, your family composition, your tax residency position in your home country, and your intended pattern of residence in Thailand. Income from employment, director's fees, or active business activities does not count toward the LTR passive income threshold — a distinction that catches many applicants by surprise.

At Warus & James Raydar Inter Law, we conduct a thorough eligibility assessment before any application is initiated, ensuring that the pathway you choose is the one you can qualify for — and the one that genuinely serves your long-term interests in Thailand and internationally.

Get Expert Guidance

Not Sure Which Visa Is Right for Your Situation?

Our initial consultation covers your full eligibility profile, income structuring, family situation, and recommended pathway — before you commit to anything.

Or email us directly at info@warusandjames.com